Key Takeaways

- The Moneylenders Credit Bureau (MLCB) records all loans issued by licensed moneylenders in Singapore, including repayment history, outstanding balances, and borrowing activity.

- Licensed moneylenders use MLCB reports to assess loan applications, determine borrowing risk, and ensure borrowers have not exceeded legal loan limits.

- The MLCB does not assign a credit score, but the data it provides can directly affect approvals, loan amounts, and eligibility for loans for bad credit.

- Maintaining timely repayments and avoiding excessive borrowing can help improve your MLCB report and strengthen future private moneylender loan applications.

- The Moneylenders Credit Bureau supports fair lending and borrower protection by preventing over-lending and promoting responsible borrowing within Singapore’s legal moneylending industry.

Have you ever wondered how a licensed moneylender decides whether to approve your loan application? Why do some borrowers get approved within minutes while others are rejected or offered a lower amount than requested?

Many borrowers in Singapore do not realise that every loan from a licensed moneylender in Singapore is recorded and may directly affect future applications. Licensed moneylenders rely on borrower data from the Moneylenders Credit Bureau (MLCB)—specifically the MLCB report—to assess repayment ability, existing debt obligations, and overall financial risk.

Whether you are applying for loans for bad credit, seeking low credit score loans, or simply trying to understand how the approval process works, knowing what the Moneylenders Credit Bureau does can help you make more informed borrowing decisions.

What Is the Moneylenders Credit Bureau?

The Moneylenders Credit Bureau is a centralised database that records all loans issued by licensed private moneylenders in Singapore. It was created to support responsible lending practices and improve transparency within the moneylender industry in Singapore.

Whenever a borrower takes out a loan from a moneylender, the details are submitted to the MLCB system. This includes information such as the loan amount, repayment schedule, outstanding balances, and repayment behaviour. Licensed moneylenders rely on this information within your MLCB report when evaluating loan applications.

Background: Moneylenders Credit Bureau

The MLCB forms part of Singapore’s regulatory framework for moneylending. It is designated by the Ministry of Law (MinLaw) and operated by Credit Bureau Singapore (CBS). Its purpose is not only to assist lenders in assessing risk, but also to help prevent excessive borrowing and encourage responsible financial behaviour among borrowers.

MLCB vs Credit Bureau Singapore

Many borrowers confuse the Moneylenders Credit Bureau with Credit Bureau Singapore, but these two credit reporting databases serve different functions.

For starters, the MLCB focuses specifically on loans issued by licensed moneylenders and private moneylenders operating legally in Singapore. Credit Bureau Singapore, on the other hand, mainly tracks borrowing activities with banks and other financial institutions, such as credit cards, personal loans, and mortgages.

When you apply for a loan from a moneylender, both systems may be relevant. For example, a licensed moneylender may review your CBS report to understand your banking-related credit obligations, while also checking your MLCB report to assess your borrowing history with moneylenders.

Because these databases track different types of borrowing, having a good record in one does not automatically guarantee a good standing in the other.

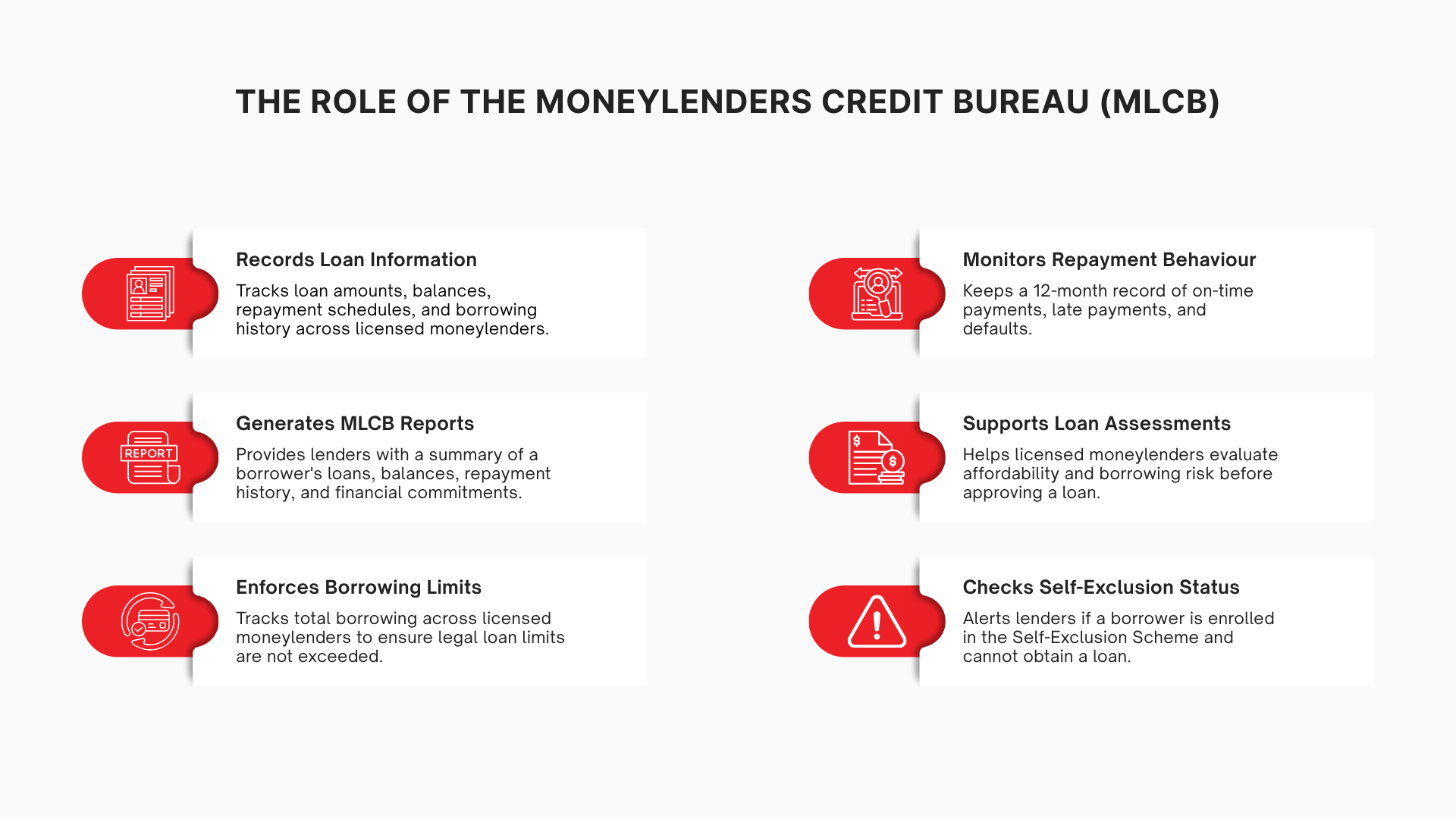

What Does the Moneylenders Credit Bureau Do?

Collects Borrower Loan Data

This creates a centralised record of borrowing activity within Singapore’s legal moneylenders’ ecosystem. By consolidating this information, the MLCB allows lenders to gain a clearer picture of a borrower’s current financial commitments before approving a new loan.

Tracks Repayment Behaviour

Late payments, defaults, and repeated missed instalments may negatively affect future applications, especially for borrowers seeking loans for bad credit or low credit score loans.

Generates Borrower Credit Reports (i.e. MLCB Reports)

The MLCB report offers valuable insight; because the system consolidates data from multiple lenders, it gives licensed moneylenders a broad overview of a borrower’s financial obligations at one glance!

Provides Data for Risk Assessment

The bureau provides factual borrowing data that allows licensed moneylenders to assess risk independently. Lenders review factors such as repayment consistency, total debt obligations, recent borrowing activity, and existing outstanding balances before deciding whether to approve a loan.

Enforces the Aggregate Loan Limit

The system tracks the total amount borrowed across all licensed moneylenders. Once a borrower reaches the legal borrowing cap, the system prevents any licensed moneylender from issuing additional loans.

Flags Self-Exclusion Status

Individuals who voluntarily enter into the Self-Exclusion Scheme are legally prohibited from obtaining loans from licensed moneylenders. The system allows lenders to verify this status before approving any application.

Why the Moneylenders Credit Bureau Is Important

The Moneylenders Credit Bureau benefits both borrowers and lenders by improving transparency within Singapore’s lending industry and creating a safer borrowing environment for consumers

For borrowers, maintaining a good MLCB report may improve their credibility when applying for a loan from a licensed private moneylender in Singapore. Strong repayment habits may increase the likelihood of approval and improve access to low credit score loans in the future.

For licensed moneylenders, the bureau supports responsible lending by helping them assess risk more accurately, comply with regulations, and avoid over-lending to borrowers who may already have excessive debt obligations.

How the Moneylenders Credit Bureau Affects Your Loan Application

When reviewing a loan application, licensed moneylenders typically examine several factors within your MLCB report.

These include:

- Your total outstanding loans

- Your repayment history over the past 12 months

- Whether you have reached your legal borrowing cap

- Any late payments or defaults

- Your self-exclusion status

For example, a borrower who consistently repays loans on time and maintains manageable debt levels is generally viewed as lower risk. In contrast, a borrower with multiple overdue accounts and high outstanding balances may face difficulties obtaining approval.

This is why repayment history plays such an important role in future applications. Like it or not, your MLCB report is telling.

How to Check Your MLCB Report

Borrowers can request their MLCB report directly through the official MLCB website.

The report currently costs S$0.50 and can usually be obtained online after identity verification. Checking your MLCB report may be useful before applying for a new loan, after paying off an existing loan, or if your recent application was unexpectedly rejected.

Reviewing your MLCB moneylender report regularly also helps you identify inaccuracies and monitor your overall borrowing position more effectively.

Tips to Maintain a Good Record With the Moneylenders Credit Bureau

Maintaining a healthy MLCB report largely comes down to responsible borrowing habits.

Paying loans on time is one of the most important factors. Even occasional late payments may affect future applications! Borrowers should also avoid taking multiple loans from different moneylenders simultaneously, as this may increase financial strain and raise concerns during risk assessments.

If you anticipate repayment difficulties, communicate with your licensed moneylender early. Many lenders are more willing to discuss alternative repayment arrangements before accounts become overdue.

It is also a good idea to review your MLCB report regularly to stay informed about your financial standing.

Common Misconceptions About the Moneylenders Credit Bureau

- One common misconception is that the Moneylenders Credit Bureau is the same as Credit Bureau Singapore. In reality, the two systems track different types of borrowing activity in Singapore.

- Another misconception is that only “bad borrowers” appear in the database. In fact, all borrowers who take loans from licensed moneylenders are recorded, regardless of repayment behaviour, loan type (e.g. loans for bad credit) and loan amount.

- Some borrowers also believe that checking their own MLCB report will negatively affect their borrowing profile. This is false. Requesting your own report does not hurt your future applications.

- Paying off a loan does not immediately erase your borrowing history. Repayment records remain visible within the rolling reporting period and may still be reviewed by lenders.

Conclusion

The Moneylenders Credit Bureau is more than just a tracking system. It serves as an important regulatory safeguard within Singapore’s lending industry by supporting fair lending, borrower protection, and debt control.

By monitoring borrowing activity and repayment behaviour, the MLCB helps licensed moneylenders make responsible lending decisions while encouraging borrowers to manage debt cautiously.

Ultimately, responsible borrowing and consistent repayment remain the most reliable ways to improve future access to loans from moneylenders. If you are looking for a trusted licensed moneylender in Singapore, 1-Cash is here to help you better understand your borrowing options and financial standing.

Apply now or contact 1-Cash today to learn more about responsible loan solutions tailored to your needs!