Key Takeaways

- Always check a moneylender’s licence through the official Registry of Moneylenders Singapore before applying for any loan.

- A licensed moneylender in Singapore must operate in accordance with the Moneylenders Act, including rules on interest rates, fees, and fair debt collection.

- Never rely on ads, social media, or reviews alone—always verify the lender’s details such as licence number, address, and contact information.

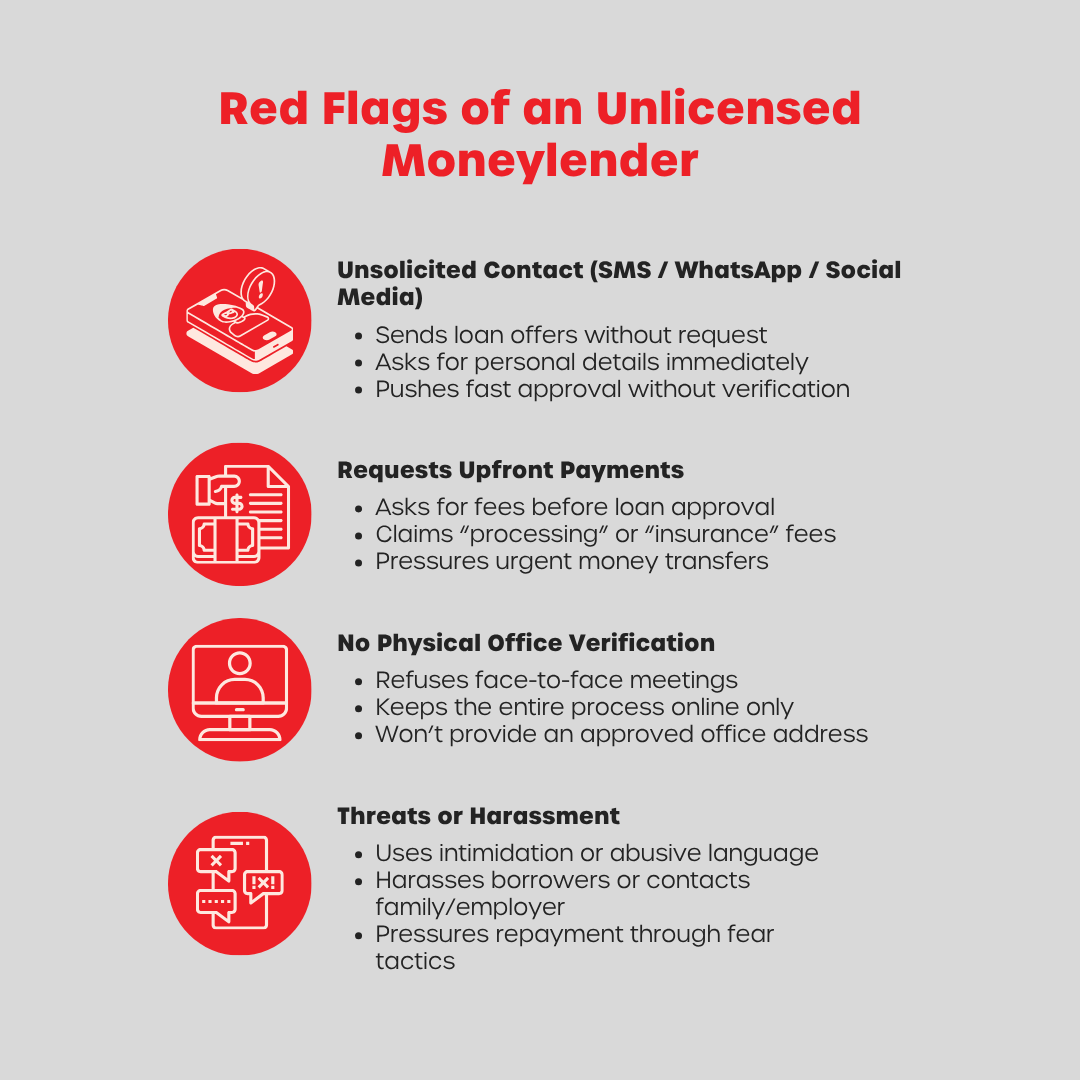

- Be cautious of red flags like upfront fees, unsolicited loan offers, remote-only approvals, or harassment tactics.

- Borrowing from an established, trusted Singapore licensed moneylender ensures better protection, transparent contracts, and regulated loan terms.

Many borrowers do not realise that it is possible—and highly recommended—to verify a moneylender’s licence before applying for a loan. While loan advertisements are easy to find online, did you know that not every lender promoting its services is legally authorised to operate in Singapore?

Taking a few minutes to check a moneylender’s licence can help you avoid scams, protect your personal information, and ensure that you are dealing with a legitimate lender. In this guide, you’ll learn how to check a moneylender’s licence, what details to look for, and why verifying a lender through the Registry of Moneylenders should always be part of your borrowing process.

Why Checking a Moneylender’s Licence Matters

Before borrowing from any moneylender in Singapore, it is important to ensure that the lender is legally authorised to operate a moneylending business.

For starters, not every lender you come across online is a legitimate licensed moneylender in Singapore. Plus, some may use misleading tactics or even blatantly impersonate established licensed companies!

This is why checking a moneylender’s licence is essential and can help you avoid illegal or blacklisted lenders before sharing personal information or signing any loan agreement.

It Helps You Avoid Illegal or Blacklisted Moneylenders

Unlicensed lenders may use aggressive, misleading, or illegal practices that place borrowers at serious risk. Verifying a lender through the Registry of Moneylenders can help ensure you are dealing with a legitimate Singapore licensed moneylender and not an illegal operator or impersonator.

It Protects You Under Singapore’s Moneylending Rules

Licensed lenders must comply with the Moneylenders Act, which regulates the lenders, loan contracts, interest rates, fees, and debt collection practices. By checking the lender’s licence status before borrowing, you can have greater confidence that the lender actually follows Singapore’s moneylending rules, and that you are entitled to the various protections available to borrowers.

How to Check a Moneylender’s Licence in Singapore

The easiest way to do this is through the Registry of Moneylenders Singapore, the official government source for confirming a lender’s licence status.

Rather than relying on advertisements, social media profiles, or third-party claims, borrowers should always refer to the registry before dealing with any moneylender to be safe!

Step 1: Visit the Official Registry of Moneylenders Website

The first step in checking a moneylender’s licence is to visit the official Registry of Moneylenders website.

The Registry maintains and updates the official list of moneylenders, making it the most trustworthy source for licence verification.

Tip: Always be cautious when searching for moneylenders in Singapore online and avoid clicking on suspicious advertisements or unofficial websites that may mimic government platforms.

Step 2: Search for the Moneylender’s Business Name

Search for the lender using its exact registered business name on the Registry of Moneylenders’ official list.

Even small differences in spelling, punctuation, or wording may indicate that the lender is not legally compliant or that someone is attempting to impersonate a licensed business. Like it or not, taking the time to verify the correct name can help prevent costly mistakes.

Step 3: Match the Details

A genuine licensed moneylender in Singapore should have details that match those listed in the registry.

Compare the lender’s:

- Licence number

- Official website

- Approved office address

- Contact number

Scammers sometimes copy the names or logos of legitimate lenders to appear trustworthy. Matching every detail against the registry can help you identify impersonation attempts before proceeding.

Step 4: Confirm That the Lender Meets You at Its Approved Place of Business

Licensed moneylenders are required to conduct face-to-face identity verification at their approved place of business before granting a loan.

If a lender claims that the entire process can be completed exclusively through WhatsApp, Telegram, SMS, or social media without any in-person verification, this is a major warning sign. Legitimate lenders must comply with all official verification requirements before approving loans.

That’s not all. All licensed moneylenders in Singapore must conduct credit checks and do their due diligence—they cannot blindly offer loans to applicants!

Step 5: Read Reviews, but Do Not Rely on Reviews Alone

A licensed moneylender’s Singapore reviews can provide useful insights into customer experiences and service quality. Such reviews may help you understand how the lender communicates with borrowers, explains repayment obligations, and handles customer enquiries.

However, reviews should always be considered a secondary source of information. Case in point, positive Singapore licensed moneylender reviews should support your decision-making process, not replace proper licence verification.

Signs You May Not Be Dealing With a Licensed Moneylender

Related read: Are You Protected From Licensed Moneylender Harassment?

Why You Should Only Borrow From Licensed Moneylenders in Singapore

Regulated Interest Rates and Fees

One advantage of borrowing from a licensed moneylender in Singapore is that interest rates and fees are tightly regulated by law.

Licensed moneylenders are generally not permitted to charge more than 4% per month in interest, regardless of income level. Late interest charges and administrative fees are also subject to legal limits. These regulations help borrowers understand the true cost of borrowing and reduce the risk of excessive charges.

Transparent Loan Contracts

Licensed lenders must provide borrowers with a written loan contract before any loan can be accepted.

The contract should clearly explain the loan amount, repayment schedule, applicable interest rates, fees, and borrower obligations. Importantly, these terms must be explained in a language that the borrower understands so that they can make informed decisions before signing.

Better Borrower Protection

Licensed moneylenders operate under the oversight of the Registry of Moneylenders and must comply with the Moneylenders Act.

If a lender breaches regulatory requirements, borrowers may report the matter to the relevant authorities. This level of oversight provides greater protection than dealing with unregulated lenders and reinforces the importance of checking a moneylender’s licence as the ultimate first step before borrowing.

Don’t Make These Mistakes When Checking a Moneylender’s Licence

Trusting Search Results Without Checking the Registry

Just because a lender appears on Google does not mean it is licensed or trustworthy. Always verify the lender through the Registry of Moneylenders Singapore rather than relying solely on search engine rankings. Knowing how to check a moneylender’s licence is essential!

Checking the Company Name but Not the Address

Scammers sometimes copy the name of a legitimate lender. To avoid impersonation scams, also compare the lender’s address, website, and contact details against the registry listing.

Relying Only on Singapore Licensed Moneylender Reviews

Customer reviews can be useful, but they should never replace official licence verification. Always confirm that the lender appears on the registry before even considering reviews.

Sharing Personal Details Too Early

Avoid providing NRIC information, Singpass credentials, banking details, or supporting documents before confirming the lender’s legitimacy. Verifying the licence first helps protect your personal information from misuse.

Is 1-Cash a Licensed Moneylender in Singapore?

Yes, 1-Cash is an established licensed moneylender in Singapore.

In addition to maintaining compliance with Singapore’s regulatory requirements, 1-Cash focuses on providing transparent loan guidance, clear explanations of borrowing terms, and customer-focused service to help borrowers make informed financial decisions.

As with any lender, borrowers are encouraged to verify 1-Cash’s registration with the official Registry of Moneylenders before applying for a loan. Checking the registry allows you to confirm the company’s licence number, approved business address, and other official details.

Conclusion

Checking a moneylender’s licence is one of the simplest yet most important steps you can take before borrowing money. By using the Registry of Moneylenders Singapore to your advantage, verifying the lender’s details properly, and remaining cautious of suspicious remote-only loan offers, you can significantly reduce the risk of dealing with illegal operators or impersonation scams.

Whether you are comparing options or preparing to apply for a loan, always take the time to confirm that the lender is properly licensed. For borrowers seeking a trusted licensed moneylender in Singapore, 1-Cash offers transparent loan terms, responsible borrowing guidance, and a straightforward application process.

Before applying for any loan, take a few minutes to check the lender’s licence legitimacy through the official Registry of Moneylenders. If you are looking for a licensed moneylender in Singapore with transparent terms, fair rates, and a convenient application process, contact 1-Cash to learn more about your options.