Key Takeaways

- Licensed moneylenders in Singapore must follow the law – They are not allowed to harass, intimidate, or publicly shame borrowers, unlike unlicensed lenders such as ah longs or loan sharks, who always do.

- Debt collection practices are regulated – Under the Moneylenders Act in Singapore and the Debt Collection Act 2022, lenders must communicate with borrowers in a professional and lawful manner at all times.

- You’re protected as a borrower – You have the right to transparent fees, a copy of your loan contract, protection from harassment, and legal avenues to report misconduct.

- Illegal lenders come with real dangers – Borrowing from unlicensed moneylenders exposes you to threats, unfair charges, and harassment, with no legal protection when things go wrong.

- 1-Cash puts responsible lending into practice – As a licensed moneylender, 1-Cash complies with all regulations, maintains transparent communication, and supports borrowers every step of the way.

Ever wondered what a licensed moneylender is allowed to do—and what’s off-limits—when collecting debts? When you borrow from a licensed moneylender in Singapore, you’re entering into a legally regulated agreement. These loans are governed by the Moneylenders Act 2008 and overseen by the Registry of Moneylenders under the Ministry of Law, which means there are clear rules that protect borrowers like you and me.

Understanding what a lender can — and cannot — do during debt collection is essential. Many borrowers are aware of illegal lenders, such as ah long moneylenders or loan sharks in Singapore, who often resort to threats or harassment to recover debts. However, the situation is very different when dealing with a legal moneylender in Singapore—they are bound by the law, treat borrowers with respect, and must not harass or pressure you.

Licensed moneylenders can take reasonable steps to recover outstanding debts and, in some cases, appoint professional debt collectors to assist them. That being said, they must always follow the law. Licensed moneylender harassment, intimidation, or any kind of abusive behaviour is strictly prohibited.

In this article, we’ll walk you through:

- How debt recovery works under Singapore law

- What licensed moneylenders cannot do

- The debt collection activities permitted under the law

- Borrowers’ rights Singapore residents should be aware of

By the end of the article, you’ll have a clear understanding of your rights and what to expect from licensed moneylenders, especially in situations where you’re unable to pay your moneylender in Singapore.

What Is a Licensed Moneylender in Singapore?

A licensed moneylender is a business legally authorised to provide loans under the Moneylenders Act 2008. Operating under strict regulatory oversight by the Registry of Moneylenders, these lenders must comply with rules governing interest rates, fees, advertising, and debt collection practices in Singapore. The first and most important step to protecting yourself from unlicensed moneylenders (colloquially known as “loan sharks” in Singapore) is knowing how they differ from licensed lenders:

Legal Moneylender |

Unlicensed Moneylender |

|

✔️ Listed on the Registry of Moneylenders ✔️ Operates from an approved place of business ✔️ Complies with interest caps and fee limits ✔️Provides written, clear contracts ✔️ Regulated under the Moneylenders Act |

❌ Not listed on the official registry ❌ Reaches out via unsolicited SMSes or messages on WhatsApp social media ❌ Charges excessive interest and illegal fees ❌ Frequently uses harassment or threats |

💡 Pro tip: Stick to licensed moneylenders if you want legal protection under the Moneylenders Act—borrowing from unlicensed lenders or loan sharks offers no legal safety net. Always verify a lender’s legitimacy by looking them up on the official list of licensed moneylenders published by the Ministry of Law.

The Legal Framework Governing Debt Collection in Singapore

Debt collection by licensed moneylenders in Singapore is governed primarily by two sets of legislation:

- The Moneylenders Act 2008

- The Debt Collection Act 2022

The Moneylenders Act in Singapore sets clear limits on interest rates, fees, and how loans must be managed. Meanwhile, the Debt Collection Act 2022 keeps third-party debt collectors in check, ensuring that debt collection practices in Singapore remain lawful and professional.

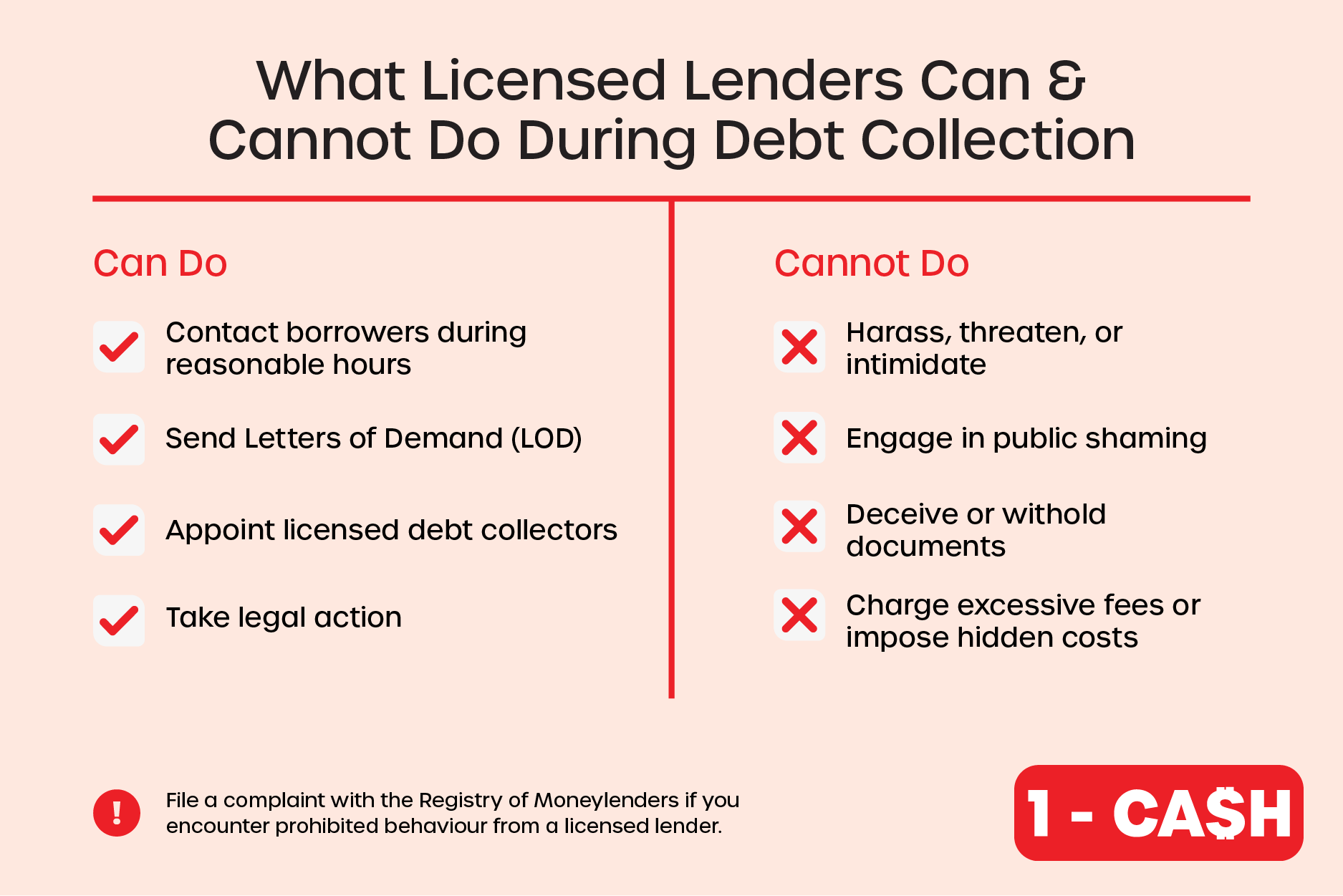

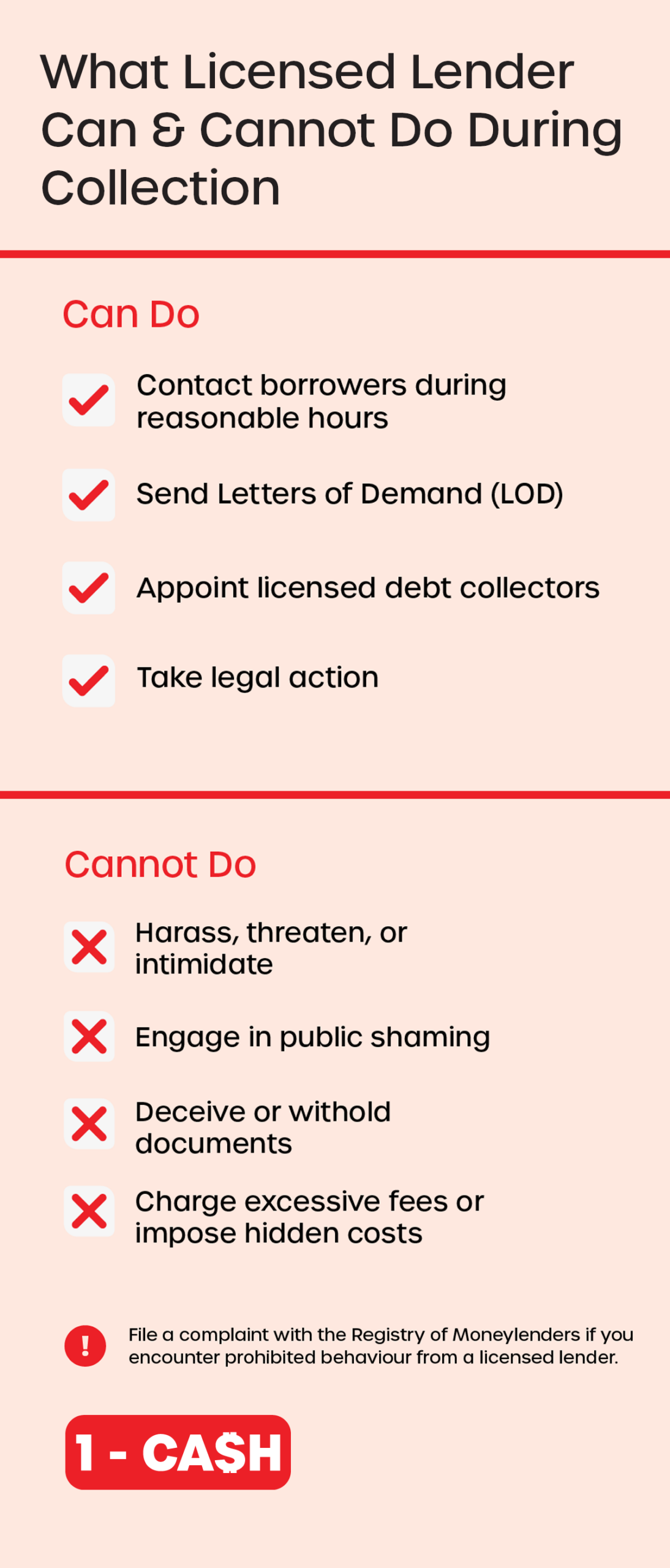

What Licensed Moneylenders Cannot Do When Collecting Debts

There are clearly defined legal boundaries that lenders must respect, even if borrowers are behind on repayments. Being aware of what a licensed moneylender cannot do empowers you to safeguard your rights:

#1 No Harassment, Threats or Intimidation

Licensed lenders cannot bully you into paying—they are strictly prohibited from threatening or imposing violence, intimidating you or your family, using abusive language, damaging property, or pressuring you with aggressive tactics.

Debt collection should never make you feel unsafe. If you experience any form of licensed moneylender harassment, know that it is unlawful—having a licence does not excuse aggressive or abusive behaviour, and lenders who breach legal standards will be subject to regulatory action.

#2 No Public Shaming

Your financial matters are private. A licensed moneylender is not allowed to paste a Letter of Demand (LOD) on your door, display your photograph, or expose your debt to neighbours or the public. They are also prohibited from posting defamatory statements or using humiliation as leverage.

Public shaming tactics are illegal. Debt recovery must remain discreet, respectful, and professional.

#3 No Deception or Withholding of Documents

Transparency is not optional—it is a requirement that applies to all licensed moneylenders under the Moneylenders Act in Singapore.

A legal moneylender in Singapore will never ask for your Singpass login credentials, retain your NRIC card, withhold copies of signed loan contracts, or use fake aliases to mislead borrowers. Remember this: you are entitled to proper documentation and clear explanations of what you owe. If something feels secretive, or if you encounter any of the above behaviours, it constitutes an infringement of borrowers’ rights in Singapore.

#4 Cannot Charge Excessive Fees or Impose Hidden Costs

Licensed moneylenders must comply with strict caps on interest rates and fees set by the Ministry of Law:

- Interest rate: Cannot exceed 4% per month

- Late interest: Maximum 4% per month, applied only to the overdue amount

- Late fee: Not more than S$60 for every month of missed repayment

- Administrative fee: Up to 10% of the principal, deducted upfront upon loan approval

- Total charges cap: The sum of the interest, late interest, late fees, and admin fees cannot exceed 100% of the principal

Licensed lenders are not allowed to impose arbitrary penalties, hidden charges, or inflated repayment balances. With these strict rules in place, borrowers are protected from falling into uncontrolled debt spirals.

#5 No Unreasonable Contact

While licensed lenders may take reasonable steps to contact you about repayment, they cannot:

- Bombard you with excessive calls

- Unnecessarily approach your employer

- Create disturbances at your workplace

- Harass your friends or family members

- Force entry into your home or workplace

Such behaviour may amount to criminal trespass or assault and should be reported immediately.

What Licensed Moneylenders Can Legally Do During Debt Collection

Licensed lenders are permitted to take lawful steps to recover outstanding debts. But how do you know what’s considered fair and legal? Here are the debt collection practices in Singapore that licensed lenders are allowed to engage in:

- Contact borrowers during reasonable hours: Typically between 8 am and 9 pm, without making excessive calls that could constitute harassment.

- Send formal Letters of Demand (LOD): These letters clearly state the outstanding amount, any applicable fees, and a repayment deadline.

- Appoint professional debt collectors: Any third-party debt collection agency must hold a licence issued by the Singapore Police Force under the Debt Collection Act 2022.

- Take legal action: Lenders can pursue debts through the Small Claims Tribunal (for amounts up to S$30,000) or the State Courts. After winning a judgment, they may apply for a Writ of Seizure and Sale to recover assets.

Whenever a debt collector is involved, the lender must provide them with accurate details:

- The total outstanding amount owed.

- A clear breakdown of interest, fees, and charges.

- The circumstances of the default, including your repayment history.

What Should You Do if Your Borrower’s Rights in Singapore Are Violated?

If you find that your borrower’s rights in Singapore have been violated by a licensed moneylender, you can take the following steps:

- File a complaint with the Registry of Moneylenders.

- Lodge a police report for criminal actions like threats, harassment, or property damage.

- Seek legal advice or protection under the Protection from Harassment Act (POHA).

When in doubt, you also have the right to ask any debt collector to provide the proof of approval from the Licensing Officer. Remember, you are protected from licensed moneylender harassment at all times.

What to Do if You’re Harassed by an Unlicensed Lender

Borrowing from unlicensed lenders—often called “ah long moneylenders” or loan sharks in Singapore—can put you in grave danger. They may charge exorbitant interest, trap you in endless debt cycles, harass you and your loved ones, damage your property, or shame you publicly.

It’s important to understand that the Moneylenders Act in Singapore only applies to licensed lenders. If an unlicensed moneylender threatens or harasses you, call 999 immediately.

To stay extra safe, always take a few moments to verify a lender’s licence before signing any agreement. Borrowing from a licensed moneylender affords you protection under the law and ensures that your loan is handled transparently and fairly.

Borrow Responsibly With Confidence

Borrowing from a licensed moneylender like 1-Cash provides you with the legal protection and peace of mind you deserve. At 1-Cash, loans are handled professionally, and you can expect respectful communication and transparent agreements—with absolutely no hidden surprises or sticker shocks.

If you’re facing difficulties with debt repayment, speaking honestly with your licensed lender can lead to constructive conversations about managing your loan. Choosing a licensed lender listed on the Registry of Moneylenders, like 1-Cash, keeps you safe from unlicensed “ah long moneylenders” who operate outside the law.

Looking for a trusted licensed lender committed to building long-term relationships based on respect and accountability? Check out our genuine client reviews or reach out to us for a non-obligatory consultation on your loan options. When you’re ready to take the next step, send in your application online—it only takes a few minutes!